Summary:

Recent concerns in private credit mostly reflect liquidity constraints and investor behavior around them. Underlying fundamentals remain generally stable as default rates normalize and institutional participation continues.

Want a broader view of this quarter’s trends? Download the full market outlook for insights across the economy, fixed income, and private markets.

Our Perspective:

We view private markets as long-duration allocations by design. Periodic dislocations can create opportunities for disciplined investors who understand (and can live with) the structure.

STRUCTURE, EXPECTATIONS, AND MISCONCEPTIONS

It’s been hard to miss the recent wave of headlines around private credit. Most of the concern clusters around two themes: limits on investor withdrawals (gating) and questions about underlying credit quality. Rising scrutiny around defaults and the durability of certain business models has pushed some investors to reassess the asset class more broadly.

But it’s worth separating the headline from the category. Much of today’s stress is concentrated in direct lending, a segment of private credit where loans are primarily backed by corporate cash flows rather than hard assets. Private credit is broader and more diverse than direct lending alone, and the debate is best framed in that narrower context.

Our view is that the narrative isn’t wrong, it’s incomplete. While pockets of risk are emerging, the larger issue is less about structural weakness and more about misaligned expectations. The tension isn’t between the assets and the vehicle. It’s between investor behavior and the long-term nature of private markets.

Private market investments are illiquid by design. Unlike public markets, where transactions clear almost instantly, private investments require time, diligence, and alignment between buyers and sellers. Liquidity isn’t continuous; it’s event-driven. Put simply: you’re not buying daily tradability; you’re earning an illiquidity premium.

In recent years, direct lending has gained traction among wealth management investors, offering yields above Treasuries, especially in a low-rate world, along with a smoother, fundamentally driven return profile.

That created a “Goldilocks” environment: strong income, low observed volatility, and the perception of periodic liquidity. Capital flowed in quickly. The Cliffwater Direct Lending Index (CDLI), a widely used proxy for U.S. middle-market direct lending, saw assets tracked in the index grow from approximately $191 billion at the end of 2021 to roughly $550 billion by year-end 2025. We’ll use the CDLI as a reference point throughout.

But capital moved faster than investor understanding. Strong performance, paired with limited experience navigating liquidity constraints, led some investors to underestimate the core trade-off: private markets require patience and are not designed to be traded tactically.

WHEN STRUCTURE MATTERED

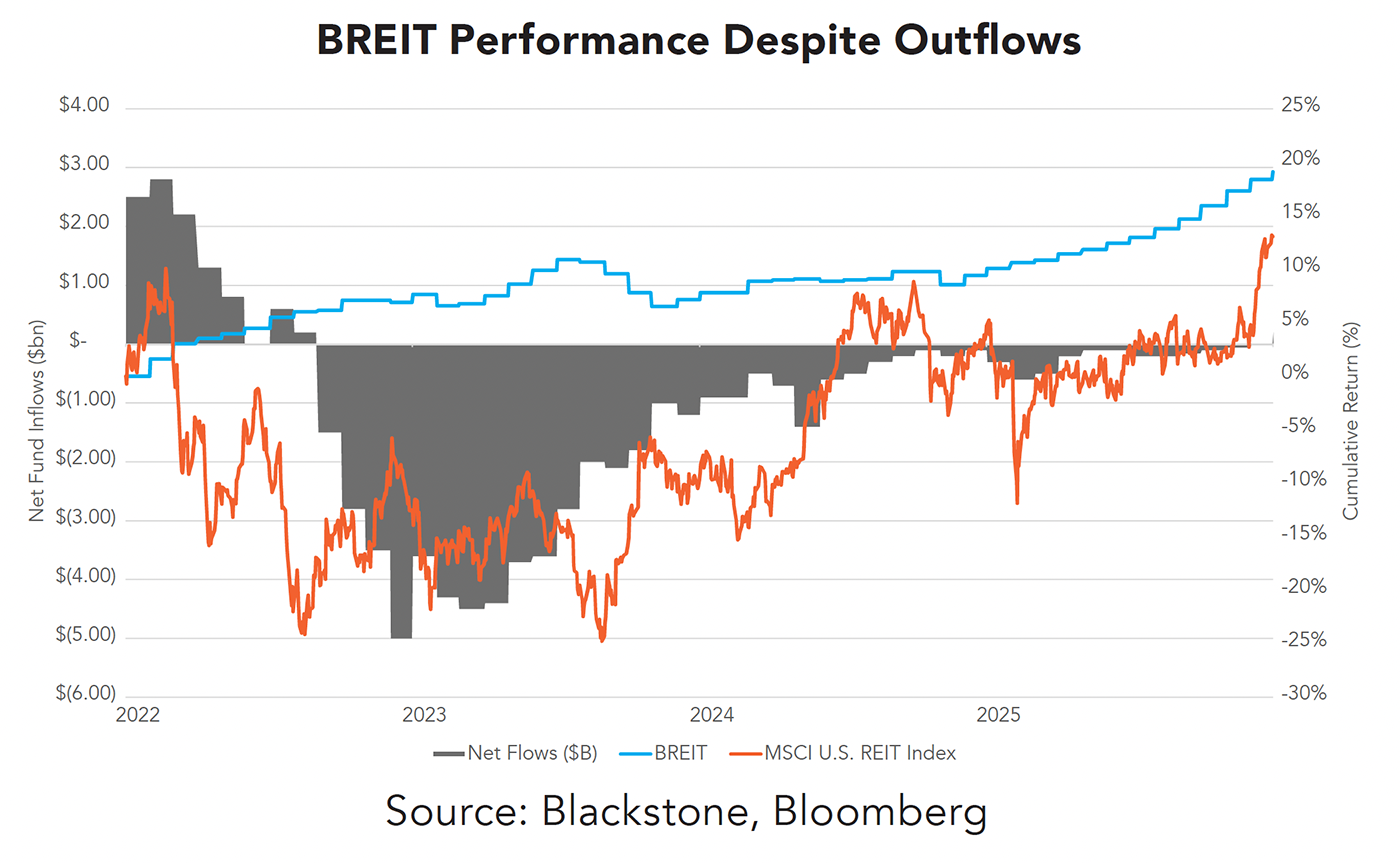

Blackstone Real Estate Income Trust (BREIT) is a useful example of how structure works, particularly in semi-liquid vehicles designed to bridge private markets with more accessible formats. BREIT offers periodic liquidity, but that liquidity is not guaranteed. In stable environments, redemptions are typically met with ease. In periods of elevated redemption demand, liquidity is intentionally constrained to protect long-term value.

In late 2022, sentiment toward commercial real estate deteriorated quickly as interest rates rose and transaction activity slowed. This coincided with many portfolios carrying an overweight to private real estate after a stretch of strong relative performance versus public markets. The result was a surge in redemption requests, driven more by narrative than realized losses.

Over the following months, requests continued to build. While the fund provided liquidity within its limits, many investors received only a prorated portion. The backlog was not fully cleared until early 2024.

From February 2022 through February 2024, BREIT generated a positive total return of approximately 8%, while publicly traded REITs declined by nearly 10%. Despite sustained redemption pressure, the portfolio remained resilient, with volatility meaningfully lower than that of public markets.

The structure allowed the manager to avoid becoming a forced seller in a weakened market, creating a buffer between short-term investor behavior and long-term asset value.

Gating is often viewed negatively, but it’s better understood as a feature rather than a flaw. It’s a circuit breaker: it prevents short-term liquidity demand from forcing the sale of long-duration assets at the wrong time. Without it, short-term decisions can become permanent losses.

WHAT IS ACTUALLY HAPPENING IN DIRECT LENDING

Recent developments in direct lending have been shaped by a rapid influx of capital. As assets expanded, competition among lenders increased, tightening credit spreads and, in some cases, pressuring underwriting discipline.

A few idiosyncratic credit events, alongside evolving risks in certain sectors (software in particular, as AI reshapes competitive dynamics), have made for easy headlines.

But the data looks more mundane than the narrative suggests. Default rates remain relatively low, with trailing four-quarter defaults near 1.5%, below the 10-year average of approximately 2.7%. Even if defaults rise meaningfully, the impact on portfolios should remain contained. Assuming implied recovery rates near 50%, a doubling of default rates would imply an annual performance drag of roughly 1.0% to 1.5%—meaningful, but not thesis-breaking given the income profile of the asset class.

Even under stressed assumptions combining higher defaults and lower recoveries, expected losses would approximate 3.5%, leaving a meaningful buffer relative to the 9–10% historical return profile.

The investor base matters, too. Direct lending remains predominantly held by institutional investors, such as pension funds and insurance companies, which account for approximately 86% of global allocations. Those investors tend to have longer time horizons and less acute liquidity needs, which helps stabilize the asset class in periods of stress.

A PERIOD OF ADJUSTMENT–AND OPPORTUNITY

We expect defaults to rise from current levels. In late-cycle environments, shaped by higher rates, geopolitical uncertainty, and technological disruption, excesses built during easier periods tend to surface.

But that adjustment can also create opportunity. As capital becomes more discerning and short-term investors step back, underwriting standards improve, spreads reset, and discipline returns. For long-term investors, these are often the conditions that produce stronger vintages.

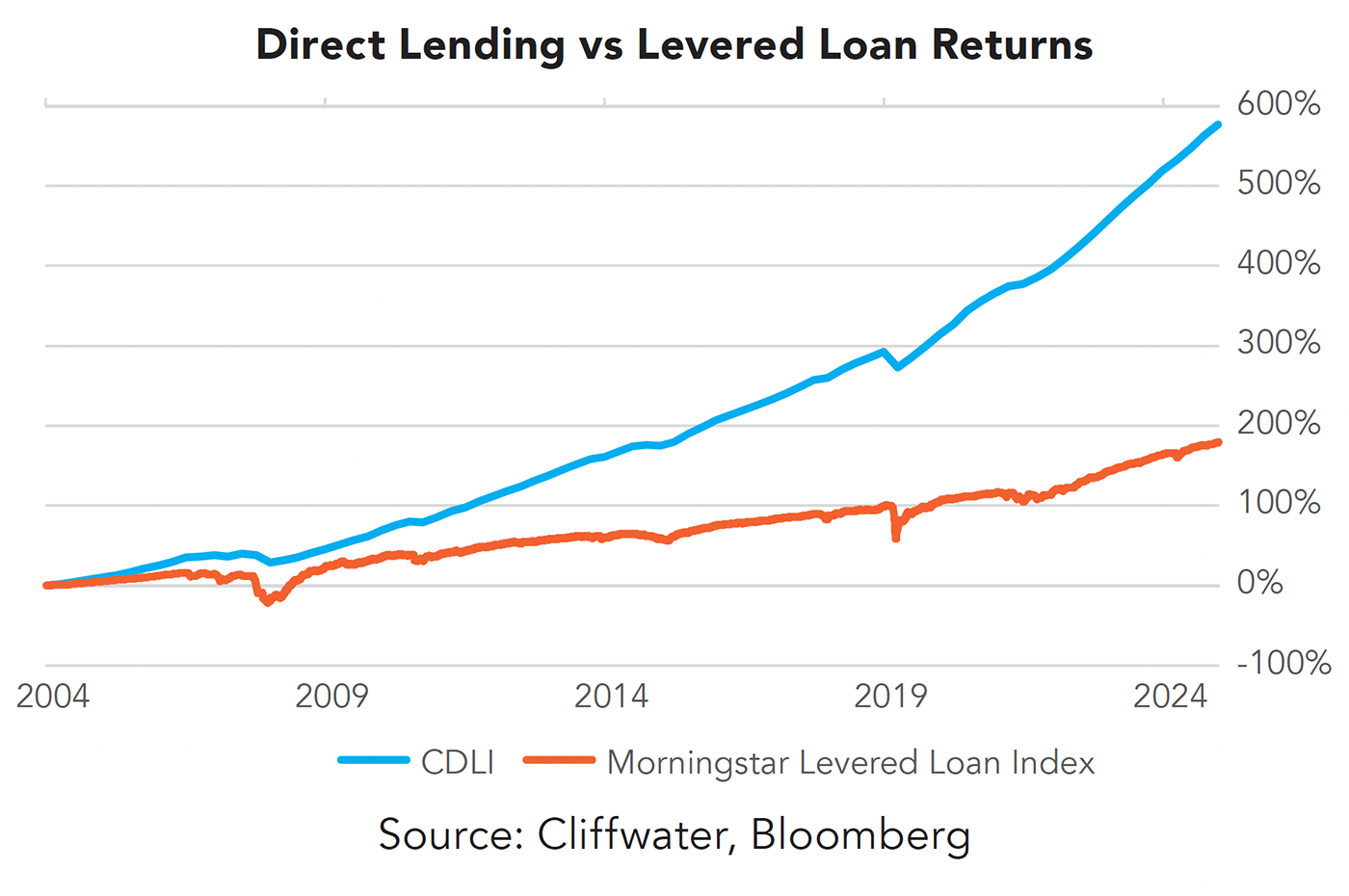

For investors who prioritize liquidity, the closest public-market analog is leveraged loans, which have historically underperformed direct lending. From 2004 through 2025, the CDLI generated a cumulative total return of approximately 576% (9.5% annualized), compared to 182% (5.1% annualized) for the Morningstar Levered Loan Index. That gap reflects the core trade-off: liquidity introduces volatility and often comes at the expense of return, meaning investors forgo the illiquidity premium over full market cycles.

It is also worth emphasizing that direct lending is only one segment of a broader opportunity set, including asset-based finance, real estate debt, and specialty lending strategies.

These evolving market dynamics may create new considerations for investors. Connect with a Midland Wealth Advisor.