.jpg?sfvrsn=3df2d46f_3)

Summary:

Geopolitical tensions and conflict have introduced a distinct risk that could disrupt energy markets and create a supply-driven economic shock. It is still too early to know how materially global growth will be affected, but it is a risk we are monitoring closely.

Want a broader view of this quarter’s trends? Download the full market outlook for insights across the economy, fixed income, and private markets.

Our Perspective:

The COVID-19 pandemic and the subsequent conflict between Russia and Ukraine exposed how fragile global supply chains can become during periods of stress. Those disruptions also spawned a wave of commentary around “onshoring,” “nearshoring,” and “friendshoring” as ways to improve resilience in critical industrial supply chains.

Those ideas look increasingly well-timed. Heading into 2026, our team identified a broadening of domestic earnings expectations as a key theme, alongside potential labor headwinds as AI tools proliferate across Corporate America.

Globally, our focus has been on the reshuffling of power and resources and what that implies for government budgets and market stability. That theme has moved to the forefront following the recent conflict in the Middle East, which has produced an unexpected energy supply shock. It forces us to reassess our initial expectations for 2026 growth, the downstream impact on consumption and borrowing, and the implications for funding markets, particularly as technology firms issue more debt to support AI-related capital expenditures.

ANOTHER MIDEAST WAR

When clients ask what our Investment Team’s role is, our answer is usually simple: risk manager first, return seeker second. That mindset shapes how we approach market outlooks and how we set expectations.

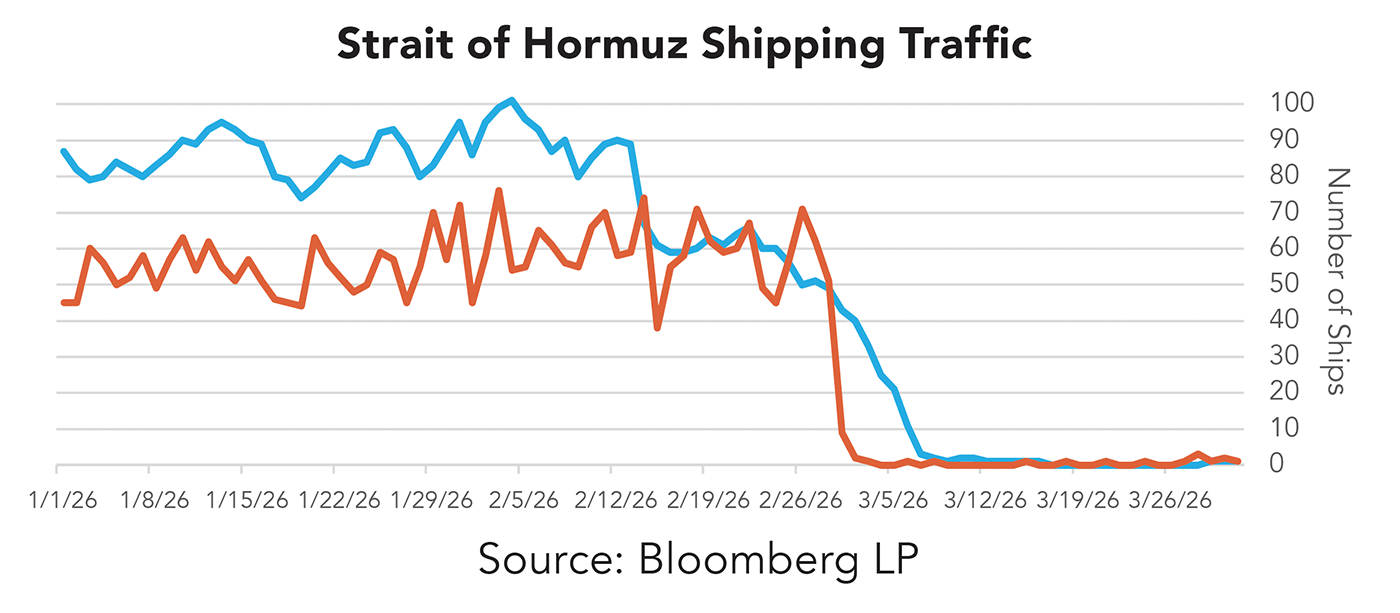

In late February, the U.S. government, alongside Israel and Gulf allies, attacked Iran during nuclear negotiations. Iran responded with missile strikes across the region and closed the Strait of Hormuz, a highly sensitive chokepoint through which roughly 20% of the world’s oil flows.

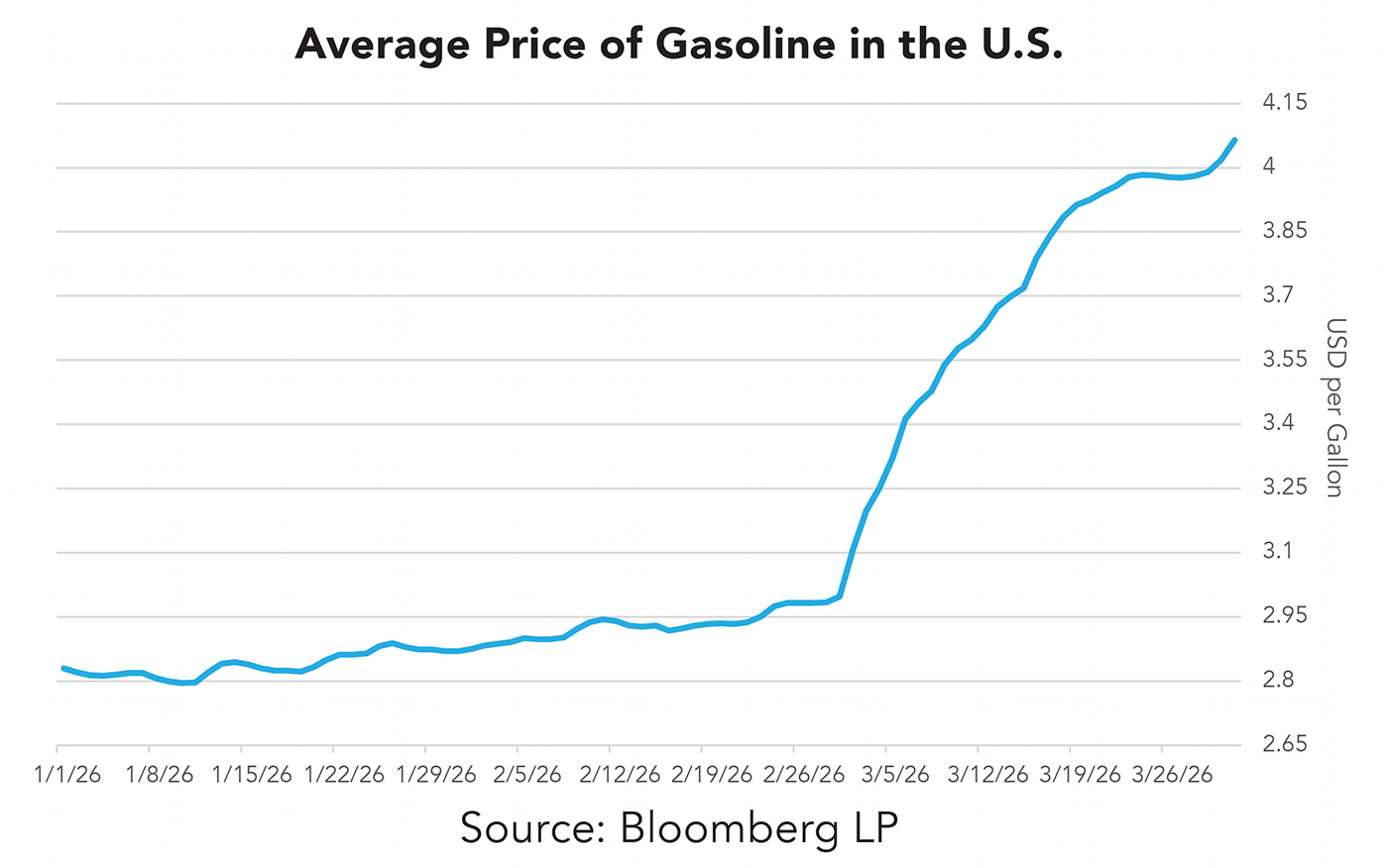

The U.S. is energy independent in the sense that we produce more energy than we consume. That does not mean the U.S. is insulated from higher oil and natural gas prices. Supply disruptions still translate into higher prices at the pump, and if those prices remain elevated long enough, they can begin to change household consumption behavior.

Wells Fargo’s economics team estimates that a sustained 50% increase in oil prices would reduce the average annual growth rate of inflation-adjusted personal consumption expenditures (PCE) by U.S. consumers by roughly one percentage point. Goldman Sachs arrives at a similar conclusion, estimating that headline PCE inflation could rise to 3.1% in its base case, while GDP growth slips modestly to 2.1% in 2026. Those forecasts assume supply disruptions last roughly six weeks—yet at the moment, the parties to the conflict appear far apart on demands.

If energy prices stay elevated, they could absorb much of what would otherwise have been a household tailwind from provisions of the One Big Beautiful Bill (OBBB) Act. In that scenario, we would likely become more cautious on domestic growth expectations.

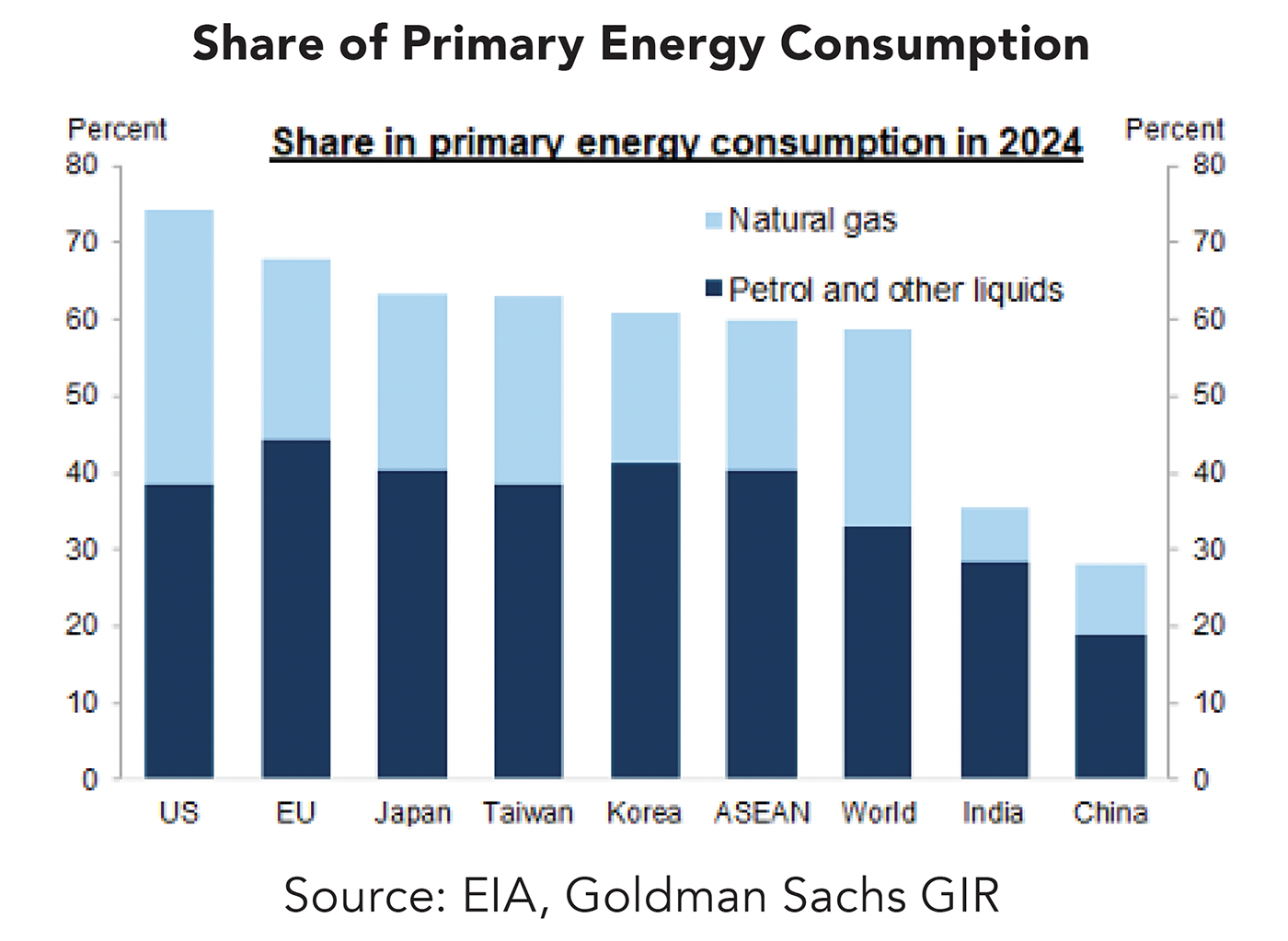

A prolonged conflict that keeps oil prices higher would likely be felt more acutely outside the U.S., particularly in the European Union, Japan, and South Korea, which import a significant portion of their energy and operate export-heavy economies. Those effects can also feed back into the U.S. through higher goods prices, keeping interest rates higher for longer and slowing progress toward additional easing by the Fed (and other global central banks). We will have more to say on this transmission mechanism and its implications for the economy and funding markets in the next section. For now, there is simply too much uncertainty and volatility to speak with precision.

AI IMPLEMENTATION AND VALUATIONS

While the Middle East conflict deserves the bulk of the discussion this quarter, we would be remiss not to address the ongoing evolution of AI and what it may mean for productivity as more firms begin implementing these tools.

The strongest evidence today points to measurable, task-level productivity gains, but not yet a broad, economy-wide step change in profits. In late 2024, the Organization for Economic Co-operation and Development (OECD) surveyed 5,000 small and mid-sized enterprises (SMEs) across Austria, Canada, Germany, Ireland, Japan, Korea, and the United Kingdom. It found that 31% of SMEs were using generative AI (likely higher today), and 65% reported improved employee performance. In the U.S., Stanford University’s AI Index reports that 78% of organizations used AI in 2024, up from 55% the year prior.

At the market level, momentum may be shifting away from the hyperscaler firms that led performance in 2024–2025 and toward small and mid-sized companies that can grow earnings faster as AI adoption improves productivity. At the same time, many firms are increasingly relying on debt markets to fund these infrastructure investments, potentially pushing costs forward and truncating future earnings growth.

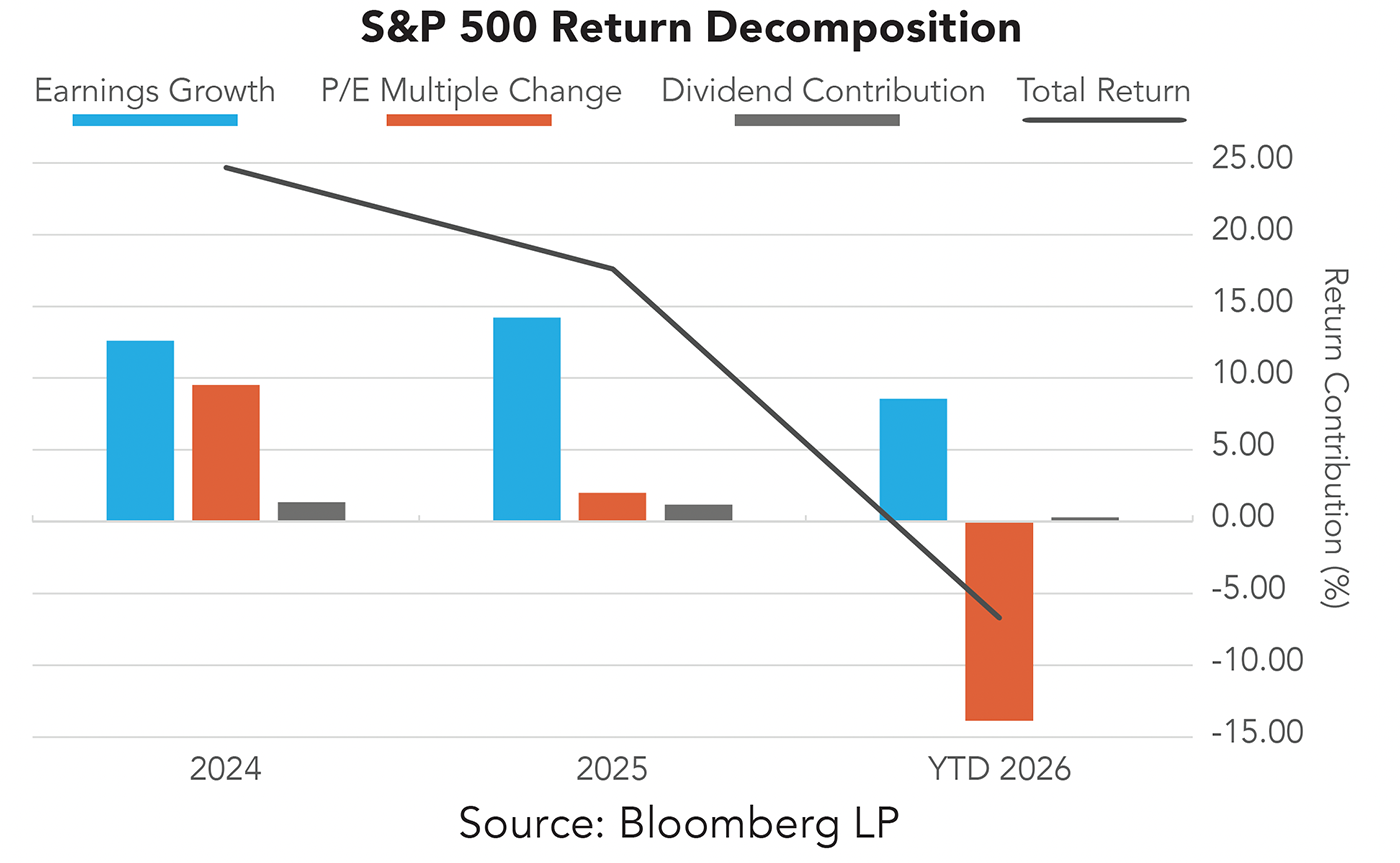

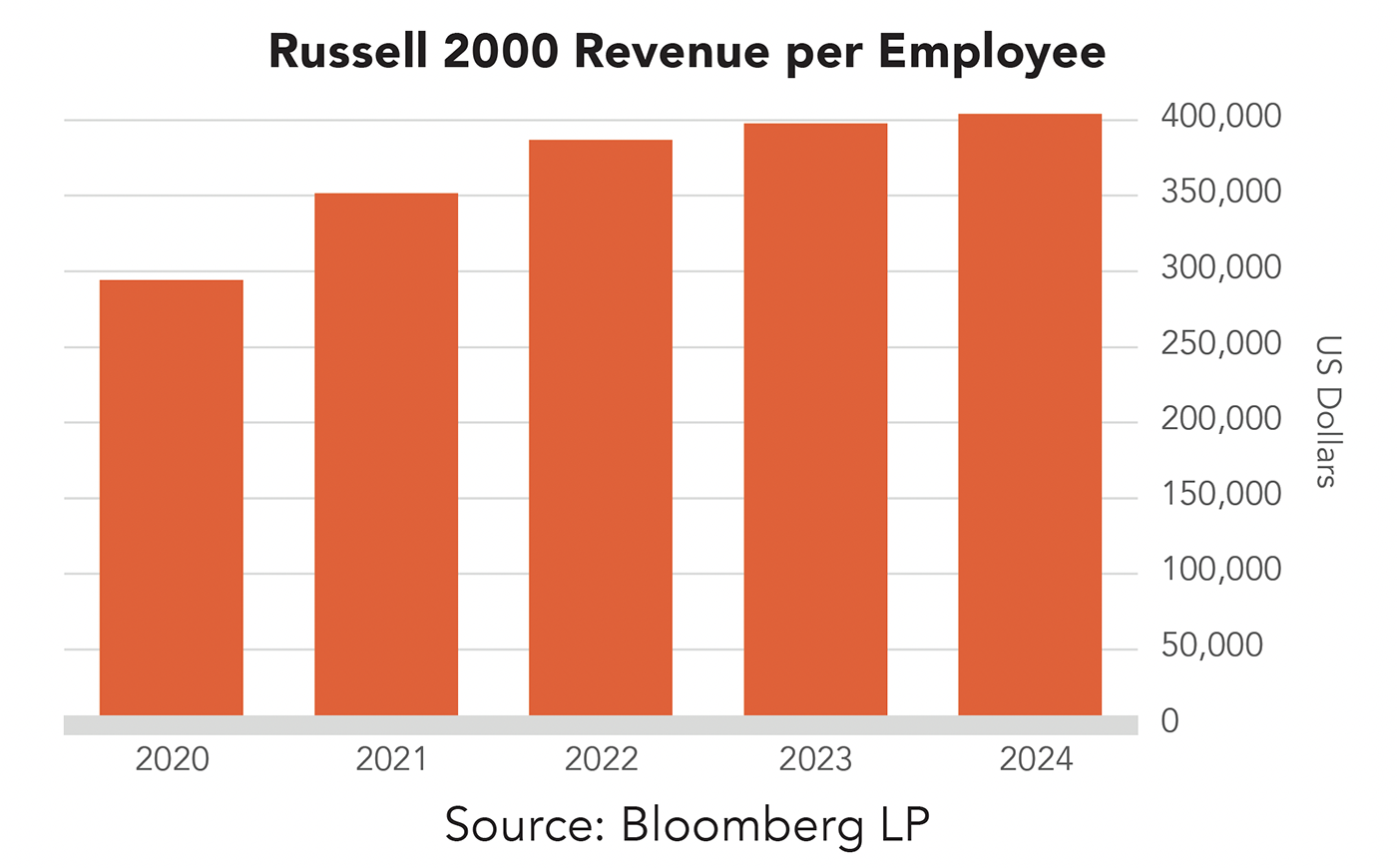

The preceding chart shows a clear shift: the S&P 500’s gains have become less about investors “paying up” for the biggest companies (which now represent roughly 30–35% of the index) and more dependent on underlying earnings delivering. In 2026, that valuation tailwind faded and is now a headwind. By contrast, productivity, measured here as revenue per employee, has been improving among smaller U.S. companies, as represented by the Russell 2000 Index, particularly since 2022 (though it is still early given incomplete annual reporting).

If earnings expectations remain resilient, small- and mid-cap equities could offer better value than large-caps did a year ago. If earnings are revised meaningfully lower, the asset class risks becoming a “value trap.” That’s why we are focused not just on valuation, but on the credibility of forward fundamentals.

As a reminder, the team recently initiated a portfolio rebalancing to reduce exposure to large-cap U.S. equities and take advantage of more favorable valuations in real estate, as well as a constructive fiscal backdrop in select emerging markets, accessed primarily through the bond market.

CONCLUDING THOUGHTS

The shift from a unipolar, U.S.-dominated world toward a bipolar or increasingly multipolar one is rooted in a simple realization: during periods of global stress, supply chains become too complex and brittle. Geopolitical competition has only reinforced that fragility.

Classical economics teaches that specialization and trade, when friction is low, can make all parties better off. But today’s geopolitical environment introduces more frequent disruptions, and therefore more volatility in growth and returns.

In this context, our priorities remain the same: risk management, sensible return objectives, and an emphasis on safety—while staying prepared to take advantage of opportunities as they emerge, both in the U.S. and abroad.

These evolving market dynamics may create new considerations for investors. Connect with a Midland Wealth Advisor.